Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Ekonomia i rachunkowość

Exercise 1

R14cnZKT9vj951

After watching the film, decide, which of the following statements are true, and which are false. Po obejrzeniu filmu, zdecyduj, które z poniższych twierdzeń są prawdziwe, a które fałszywe.

Prawda

Fałsz

A new employee asks a more experienced colleague to help him implement himself to work here.

□

□

The new employee doesn’t know much about the documents, even in theory.

□

□

The new employee dealt with documents at his previous job.

□

□

They use a good document service application here.

□

□

The GRN document is used when purchasing goods and with their free of charge acceptance.

□

□

The GRN document is issued on the basis of an invoice only.

□

□

The new employee will most definitely never encounter the Internal goods receipt note.

□

□

The goods dispatch documents register the material turnover in the warehouse.

□

□

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 2

R8wvb5X54bHH91

Ekonomia i rachunkowość

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 3

R14FH8YDwLXiJ1

After watching the film, match Polish phrases with their translations. Po obejrzeniu filmu, połącz polskie frazy z ich tłumaczeniami.

wydanie na zewnątrz, rozchód wewnętrzny, nieodpłatne przyjęcie, zwroty wewnętrzne, zwiększanie ilości, towar na stanie, przyjęcie zewnętrzne, system magazynowy, przyjęcie wewnętrzne, obrót materiałowy

goods received note

free of charge acceptance

internal goods receipt note

increase in the quantity

goods in stock

return of stock

material turnover

external dispatch

internal dispatch

warehouse system

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

m7e5d30f9aa1f828a_1534958755277_0

STAGES OF THE SUPPLY PROCESS

R7NidUTBHWQbW1

Ekonomia i rachunkowość

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Ekonomia i rachunkowość

Exercise 4

Rlu3MJUSfxNb31

After watching the voiced animation, arrange the supply process stages in the right order. Po obejrzeniu animacji z lektorem, uporządkuj etapy procesu zaopatrzenia w odpowiedniej kolejności.

monitoring the course of the order

selection of suppliers, negotiation of the terms of the order

summary of stock reports, decision, internal exchange of goods, ordering procedure

contact with the warehouse

determining the assortment and quantity of the ordered goods

acceptance of the plan, placing an order

filing a complaint, detecting irregularities, completed orders

contact with the shipping department

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 5

R1RpNc3X4IqBe1

After watching the voiced animation, fill in the gaps in the sentences with correct prepositions. Use the word bank. Po obejrzeniu animacji z lektorem, uzupełnij luki w zdaniach odpowiednimi przyimkami. Skorzystaj z banku słów.

on, of, into, with, in, out, by, for

Supply is one ............ the essential processes in a company.

Stock control prevents any shortages ............ it.

You can divide the process ............ stages.

It has a potential for carrying ............ orders of various size.

The next stage is the contact ............ the shipping department.

It can be omitted if the shipping is handled ............ the supplier.

At this stage, the person responsible ............ the orders contacts the warehouse manager.

At the next stage a report ............ the course order is created with a list of suppliers.

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 6

RwDAJAmHAzdqr1

After watching the voiced animation, match Polish phrases with their translations. Po obejrzeniu animacji z lektorem, połącz polskie frazy z ich tłumaczeniami.

wymiana towaru, kontrola zapasów, sytuacja finansowa, terminowość dostaw, sposób rozliczenia, plan zamówienia, zestawienie raportów, warunki zamówienia, procedura zamawiania, wykryć niezgodności

timeliness of deliveries

stock control

report summary

goods exchange

order procedure

terms of the order

financial situation

procurement plan

settlement method

discover irregularities

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

m7e5d30f9aa1f828a_1534958767204_0

CORRECTION OF WAREHOUSE DOCUMENTS

HR: Hi. I have a request for you. We are preparing materials for e‑learning for new employees. I would like you to write a part related to the correctionm7e5d30f9aa1f828a_1535289197378_0correction of warehouse documentsm7e5d30f9aa1f828a_1535289213182_0warehouse documents.

E: I think that someone from the bookkeeping would be better for writing this.

HR: We care about an employee perspective. The material will still be checked.

E: In general, I would start with the types of corrections. A reminder that we distinguish three such types.

HR: If you want, we can write it down right away.

E: Alright. So we have three types - quantitative correctionsm7e5d30f9aa1f828a_1535289210555_0quantitative corrections - that is, issued for most documents. This applies to both warehouse and trade documents. They usually refer to the reduction of the quantity of goods from the corrected documentm7e5d30f9aa1f828a_1535289207593_0corrected document, i.e. returns. You can also issue documents that increase the amount of goods. These are so‑called positive adjustment.m7e5d30f9aa1f828a_1535289204203_0positive adjustment.

HR: As next, we will discuss the value correctionm7e5d30f9aa1f828a_1535289192388_0value correction?

E: Yes. Write down that it relates to a change in the valuem7e5d30f9aa1f828a_1535289189053_0change in the value of the goods relative to the document being corrected.

HR: The third point will be the correction of the VAT ratem7e5d30f9aa1f828a_1535289184205_0correction of the VAT rate.

E: Exactly. I see that you could write it yourself.

HR: I know a little.

E: Add that the errors in the warehouse documents can be corrected in two ways - through the corrective documentm7e5d30f9aa1f828a_1535289207593_0corrective document issued by the seller and the correction notem7e5d30f9aa1f828a_1535289173734_0correction note. The buyer prepares it.

HR: Then maybe we will write a little about the corrective note?

E: Hmm. I think it is worth pointing out how it differs from the correcting document. The corrective note is issued only by the buyer in the case of defects that do not concern the amounts appearing in the original document.

HR: Maybe we can add a point about what a corrective note cannot apply to?

E: A good idea. There are interesting cases here. Please also note that it requires the approval of the issuer of the warehouse document it concerns.

HR: Alright. Write down the most common errors appearing on the corrective notes. Enough for today. Thank you very much.

E: No problem. See you later.

HR: See you.

Exercise 7

R1Rlniolfyj9e1

Ekonomia i rachunkowość

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

m7e5d30f9aa1f828a_1535289197378_0

korekta

R34Jw3X1yONoo1

Ekonomia i rachunkowość

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Ekonomia i rachunkowość

Exercise 8

RdmM73ICRcuAz1

After listening to the audio recording, fill in the gaps in the sentences. Use the word bank. Po wysłuchaniu nagrania audio, uzupełnij luki w zdaniach odpowiednimi słowami. Skorzystaj z banku słów.

The interview is about choosing the right .............................................

It is important to do the ............................................ based on past data helps to avoid mistakes and show new shopping possibilities.

The company tries to choose criteria that will allow it to minimise the ............................................ of making a mistake.

Focusing on time is mainly focusing on whether the supplier ............................................ or is able to meet urgent orders.

It is also important to know the extent to which our contractor is willing to ............................................ the amount of rebates.

It was also important whether they provide price ............................................ in the long run.

The company ............................................ checks the standards that the supplier meets, the quality control system, the guarantees given.

Issues related to the possibility and conditions of ............................................ are also important.

A breakthrough in the approach to suppliers was the introduction of checking their ............................................ situation.

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 9

RwvKnBdw1AcTl1

After listening to the audio recording, choose the correct article. If no article is necessary, choose “-”. Po wysłuchaniu nagrania audio, wybierz prawidłowy rodzajnik. Jeśli nie potrzeba żadnego rodzajnika, wybierz “-”.

-, the, the, a, -, the, -, the, the, a, a, a, the, a, -, a, -, an, -, -, -, the, a, the

Today we will talk about choosing ............ right contractor.

We have ............ expert in our studio.

Suppliers analysis based on ............ past data helps to avoid mistakes and show new shopping possibilities.

Through years of ............ practice, we have tried to choose various criteria.

Initially, we mainly focused on ............ time.

It was also important whether they provide price stability in ............ long run.

It happened to us that ............ permanent supplier suddenly ended cooperation due to liquidity problems.

And it is ............ last factor that should be mentioned.

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

Exercise 10

R1S985RzYSWTG1

After listening to the audio recording, match Polish words and phrases with their translations. Po wysłuchaniu nagrania audio, połącz polskie terminy z ich tłumaczeniami.

warunki reklamacji, sytuacja finansowa, możliwości zakupowe, normy, wysokość rabatu, negocjować, dotrzymywać terminów, system kontroli jakości, analiza dostawców, stabilność ceny

suppliers analysis

shopping possibilities

meeting deadlines

amount of rebates

negotiate

price stability

standards

quality control system

conditions of complaint

financial situation

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

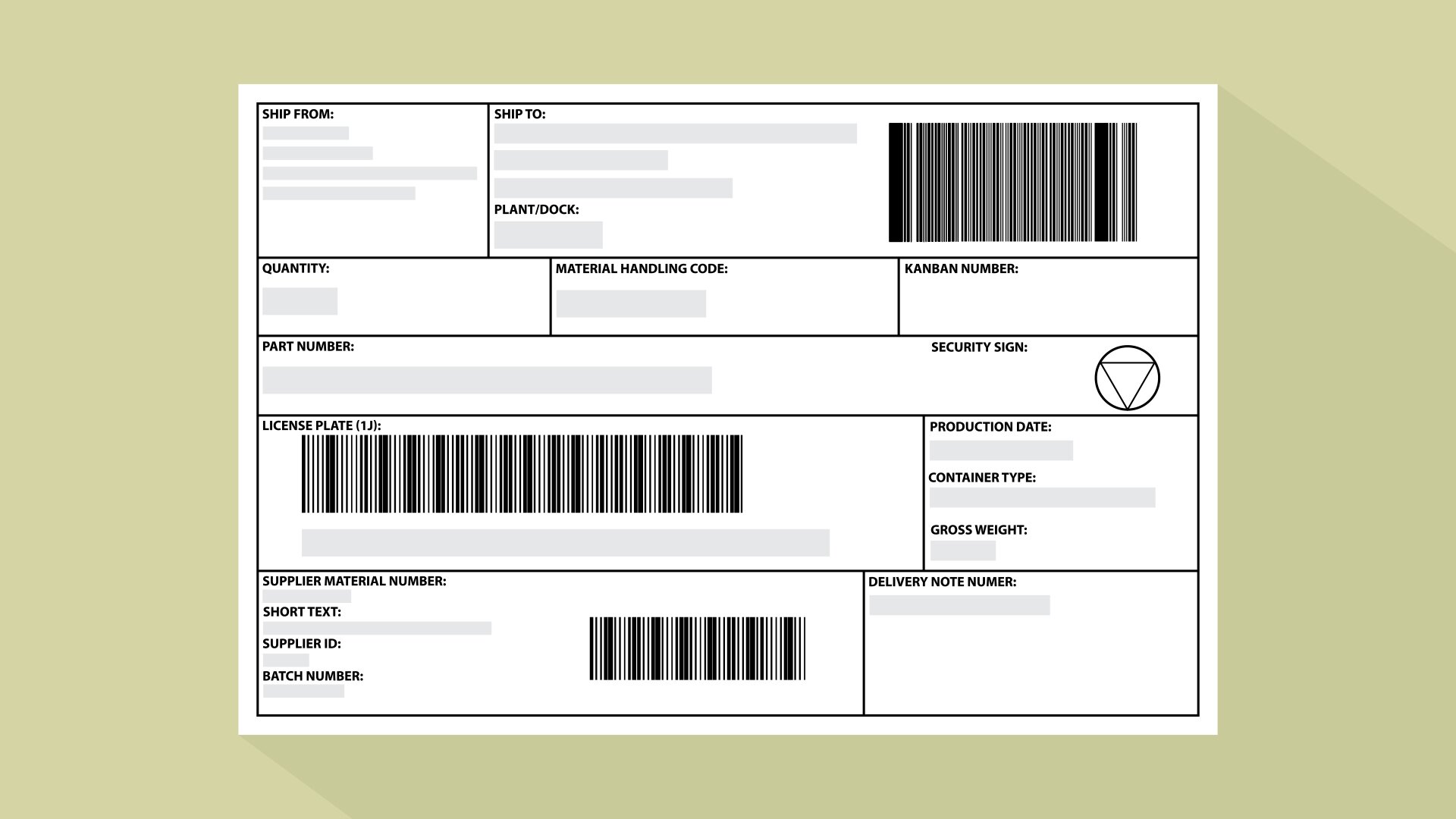

m7e5d30f9aa1f828a_1534958820248_0

GOODS DISPATCH NOTE

R15f8TzJmn0Js1

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

m7e5d30f9aa1f828a_1534958839011_0

Pictures

R198UHbRJOeWi1

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

REpAqnMNAPvUS1

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.

R11PDQq6zoXJ91

Ekonomia i rachunkowość

Source: Instytut Technologii Eksploatacji / Funmedia, cc0.